Table of Content

For example, if youre planning on a home renovation, you can borrow new funds for each step of your project, rather than as a single lump sum. Schedule an appointment with a loan officer today to get started. You can also look online for rates to compare lenders with your current mortgage lender prior to fully applying for a HELOC. You may want to complete online prequalification with a few lenders, which can give you a sense of the terms and rates theyre offering, as well as the fees theyll charge. The IRS grants an exclusion on real-estate capital gains up to $500,000 for married couples filing jointly, and $250,000 for singles .

Although other requirements exist, only the interest you actually pay during the year is eligible for a deduction. If you make a late mortgage payment in the following tax year, you must wait until that year to claim the deduction. You must use the loan to perform substantial renovations. Any loans taken out before the TCJA must still follow the current qualification rules. So, if you deduct interest on loans used to pay for things like tuition or medical expenses in the past, you cant take that same deduction this year, so be prepared for that. From 2018 until 2026, interest on home equity loans and HELOCs is only tax deductible if the borrower uses the proceeds to buy, build, or substantially improve the home that secures the loan.

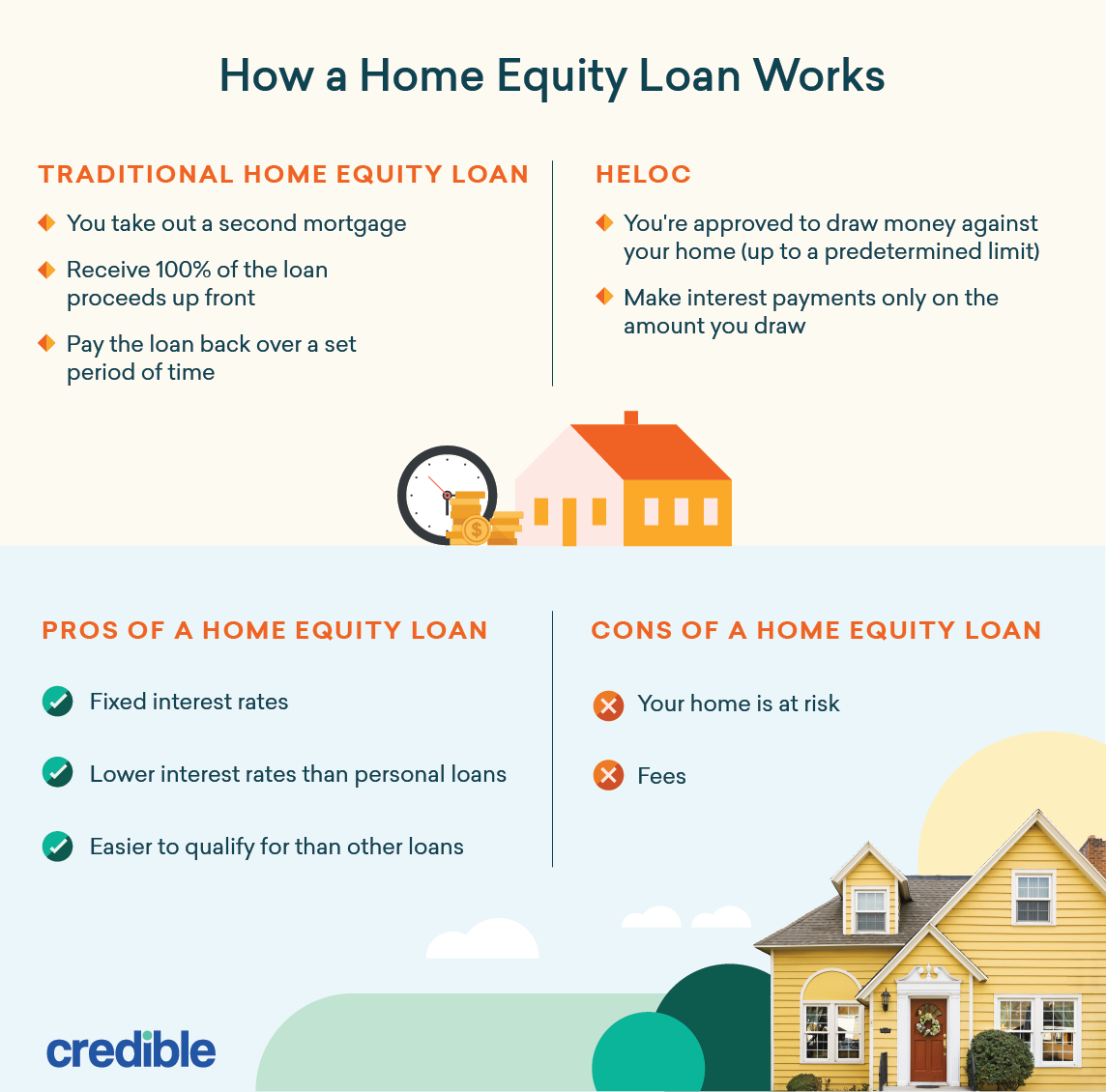

Home Equity Loans Basics

You should receive IRS Form 1098 from your lender with details about the interest you've paid on your home equity loan. Of Schedule A (Form 1040.) Any non-tax deductible interest paid on a home equity loan needs to be reported on line 8b. As a result of the Tax Cuts and Jobs Act enacted in 2017, the deduction works differently in tax years 2018 and beyond compared to years prior. However, if you use the proceeds of the loan for what the IRS deems to be "substantial improvements" to your home, and meet other criteria, home equity loan interest may still be deductible to an extent.

Generally, this information is included on the settlement statement you get at closing. Most state and local governments charge an annual tax on the value of real property. You can deduct the tax if it is assessed uniformly at a like rate on all real property throughout the community. The proceeds must be for general community or governmental purposes and not be a payment for a special privilege granted or special service rendered to you. To prevent taxpayers from claiming a deduction for luxurious homes, the law limits the deduction to the interest that you pay on up to $750,000 in total mortgage balances.

Tax Deductions on Home Equity Loans and HELOCs: What You Can (and Can’t) Write Off

Receives at least 80% of its gross income for the year in which the mortgage interest is paid or incurred from tenant-stockholders. For this purpose, gross income is all income received during the entire year, including amounts received before the corporation changed to cooperative ownership. If you received a refund of mortgage interest you overpaid in an earlier year, you will generally receive a Form 1098 showing the refund in box 4. If you prepaid interest in 2022 that accrued in full by January 15, 2023, this prepaid interest may be included in box 1 of Form 1098. However, you can't deduct the prepaid amount for January 2023 in 2022. (See Prepaid interest, earlier.) You will have to figure the interest that accrued for 2023 and subtract it from the amount in box 1.

If you claim an adoption credit for the cost of improvements you added to the basis of your home, decrease the basis of your home by the credit allowed. This also applies to amounts you received under an employer's adoption assistance program and excluded from income. For more information, see Form 8839, Qualified Adoption Expenses. Figure the part of the federal gift tax paid that is due to the net increase in value of the home by multiplying the total federal gift tax paid by a fraction. The net increase in the value of the home is its FMV minus the adjusted basis of the donor.

You Can Only Deduct A Certain Amount

Armed Forces and qualified veterans may use MilTax, a free tax service offered by the Department of Defense through Military OneSource. For more information go to MilitaryOneSource (MilitaryOneSource.mil/Tax). Remove from this record any improvements that are no longer part of your main home. For example, if you put wall-to-wall carpeting in your home and later replace it with new wall-to-wall carpeting, remove the cost of the first carpeting. If a public utility gives you a subsidy for the purchase or installation of an energy conservation measure for your home, don’t include the value of that subsidy in your income.

Discharges of qualified principal residence indebtedness. Mortgage interest deductions are only available to taxpayers who itemize deductions on a Schedule A attachment to their Form 1040. However, you can choose any second home to qualify for the deduction. Whichever second home you choose is only binding for the current tax year. Next year, you can deduct the mortgage interest on a different second home if it provides greater tax savings. For example, the maximum credit for expenses relating to adoption will be raised to $14,080.

Since the collateral is your home, interest rates are lower than other consumer loans or credit cards. So, let's say you're single and between your various deductions, you have a total of $13,500 in write-offs for your 2021 tax return. But if you're only at $10,000 between your various deductions, then that means you're better off choosing the standard deduction -- even if it means forgoing a write-off for the interest you paid on your home equity loan.

If you pay off your home mortgage early, you may have to pay a penalty. You can deduct that penalty as home mortgage interest, provided the penalty isn't for a specific service performed or cost incurred in connection with your mortgage loan. Interest paid on home mortgage proceeds is only deductible to the extent the loan proceeds were used to buy, build, or substantially improve your home. You can only deduct home mortgage interest to the extent that the loan proceeds from your home mortgage are used to buy, build, or substantially improve the home securing the loan.

The loan must be secured by the taxpayer’s main home or second home , and meet other requirements. In addition to limiting the deduction to certain expenses, the interest deduction is only available for a total loan amount of $750,000. This means that if you are claiming the mortgage interest deduction for both your primary mortgage and your home equity loan or HELOC, you can only claim interest on up to $750,000 of combined loan balances.

The loan can be a first or second mortgage, a home improvement loan, a home equity loan, or a refinanced mortgage. Your deduction for home mortgage interest is subject to a number of limits. If one or more of the following limits applies, see Pub. 936 if you later refinance your mortgage or buy a second home. You and the seller each are considered to have paid your own share of the taxes, even if one or the other paid the entire amount. You each can deduct your own share, if you itemize deductions, for the year the property is sold.

You may not receive this form if you paid less than $600 in interest. This indebtedness is a mortgage that you took out to buy, build, or substantially improve your principal residence and that is secured by that residence. You may be able to take an itemized deduction on Schedule A , line 8d, for premiums you pay or accrue during 2021 for qualified mortgage insurance in connection with home acquisition debt on your qualified home.

Enter the result as a decimal amount 14.× .15.Multiply the amount on line 13 by the decimal amount on line 14. Otherwise, you can use Table 1 to determine your qualified loan limit and deductible home mortgage interest. All of the interest you paid on grandfathered debt is fully deductible home mortgage interest. However, the amount of your grandfathered debt reduces the limit for home acquisition debt.

No comments:

Post a Comment